VA Streamline Refinance: How It Works and When to Get One

Our goal is to give you the tools and confidence you need to improve your finances. Although we receive compensation from our partner lenders, whom we will always identify, all opinions are our own. Credible Operations, Inc. NMLS # 1681276, is referred to here as “Credible.”

If you’re a veteran with a VA home loan, there’s a simple way to refinance that could save you money.

A VA streamline refinance — or VA interest rate reduction refinance loan (IRRRL) — may be able to lower your interest rate, shorten your mortgage term, or shrink your monthly payment, often with no appraisal or credit underwriting.

Here’s what you need to know about VA streamline refinances:

What is a VA streamline refinance (VA IRRRL)?

If you’re an active-duty military service member, veteran, or surviving spouse with a VA mortgage, you might be thinking about refinancing to lower the interest rate on your current home loan.

An IRRRL can help you accomplish this by replacing your existing VA loan with a new one that has a different interest rate and monthly payment, and possibly a different term.

What makes this refinance “streamlined” is that it typically requires fewer steps and less paperwork. For instance, the VA doesn’t require an appraisal or credit underwriting for this loan, which means you’ll usually close faster than someone doing a conventional refinance.

Learn More: How Soon You Can Refinance: Typical Waiting Periods By Home Loan

VA streamline refinance rates

Veterans United, a major originator of VA loans, says that the interest rates on VA loans tend to be 0.5% to 1.0% lower than the interest rates on conventional mortgages. And lending statistics from ICE Mortgage Technology show that from January through August 2021, VA loan rates were about 0.3 percentage points lower than conventional loan rates on a 30-year, fixed-rate mortgage.

Rates also vary by mortgage lender, loan term, and how much home equity you have. For example, if you have at least 20% equity and can pass underwriting and an appraisal, you might find a better interest rate and lower APR by refinancing into a conventional loan, even if you qualify for an IRRRL.

Getting pre-approved with multiple lenders will give you the best idea of what rates you qualify for. It’ll also allow you to compare loan costs and get a taste of the lender’s customer service before committing to the mortgage approval process. While Credible doesn’t offer VA streamline refinances, we can help you find a great rate if you’re refinancing a conventional loan.

Find My Refi Rate

Checking rates will not affect your credit

VA streamline refinance loan benefits

A VA streamline refinance has several appealing advantages:

- Competitive rates: VA loan rates tend to be similar to or slightly less than conventional loan rates.

- No private mortgage insurance: Even with less than 20% equity, there’s no PMI or equivalent for VA loans like there is for conventional loans and FHA loans.

- No appraisal: A no-appraisal refinance will save you a few hundred dollars in upfront costs. It also means you may be able to refinance a home that’s lost value.

- Less documentation: A VA streamline refinance doesn’t require underwriting, so you may be able to forgo gathering bank statements and tax returns for lenders.

- Closing cost financing: Avoid out-of-pocket costs by rolling closing costs into your new loan.

- Quick closing: No underwriting and no appraisal means it likely won’t take as long to refinance your home.

- No occupancy requirement: You can do a streamline refinance on a home you no longer occupy as your primary residence.

- Catch up if you’ve fallen behind: If your VA loan is past due, you may be able to use an IRRRL with credit underwriting to catch up on overdue payments, pay off late fees, and get into a more affordable loan that will stabilize your situation.

Drawbacks of VA streamline refinance loans

Even though a VA streamline refinance is meant to be money-saving and efficient, you should understand how its drawbacks might affect you:

- Funding fee: You’ll pay a funding fee each time you get a VA loan. The fee is 0.5% of the loan amount for an IRRRL.

- Existing VA loan required: If you have a conventional loan or FHA loan, you’re not eligible for an IRRRL. However, you may qualify for a VA cash-out refinance.

- Closing costs: Expect to pay fees for loan origination, title insurance, and local government requirements.

- Restarting your loan term: Many borrowers choose the same loan term when they refinance. If you currently have a 30-year loan that you’ve been paying for four years, you’ll be mortgage-free in 26 years. But if you refinance into a new 30-year loan, you’ll have to start over.

- No cash out: Borrowers are not allowed to cash out any equity with an IRRRL unless the money is a reimbursement for energy-efficient home improvements completed within 90 days of closing and costing no more than $6,000.

- Waiting period: You’re not eligible for an IRRRL until you’ve had your existing VA loan for 210 days and made six consecutive monthly payments.

Compare Your Options: 3 Ways to Refinance a VA Loan

VA streamline refinance eligibility guidelines

Qualifying for a VA streamline refinance can be easier than qualifying for other refinance loans. Here are the key criteria and a brief explanation of each one:

| Requirement | Description |

|---|---|

| You’re refinancing a VA loan | You can’t use a VA IRRRL to refinance a conventional, FHA, or USDA loan. |

| You’re no more than 30 days behind on payments | If you’re more than 30 days behind, you’ll have to go through underwriting. |

| The home has been your primary residence | It’s OK if your home is not your primary residence anymore or won’t be after you refinance, as long as it was previously. |

| Your new loan won’t push back your payoff date by more than 10 years | For example, if you have 12 years left on your VA loan, your new loan term can’t be longer than 22 years. That means you wouldn’t be able to refinance into a 30-year loan. |

| Your new loan will have a lower interest rate | One exception: You can refinance into a higher rate if you’re refinancing an adjustable-rate mortgage (ARM). |

| You don’t want to cash out any equity | There’s no cash-out refinance option with an IRRRL. Look into a VA cash-out refinance instead. |

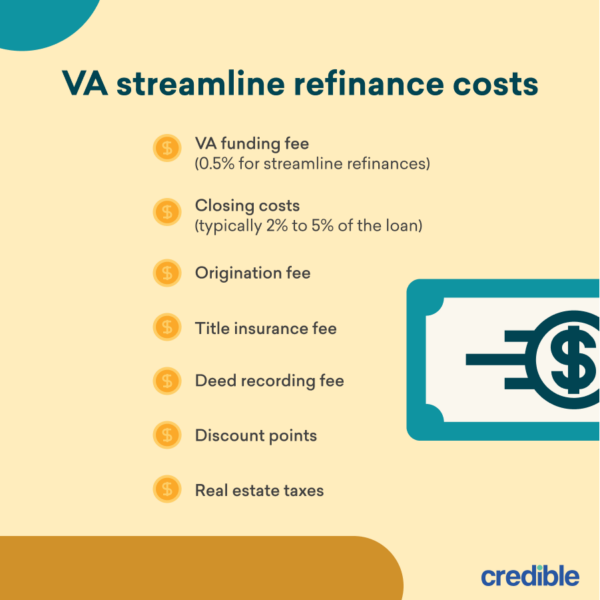

VA IRRRL costs

The closing costs for a VA streamline refinance are similar to the closing costs for other VA loans. However, you likely won’t have to pay for an appraisal, which will save you a few hundred dollars. Here are some of the closing costs often associated with a VA IRRRL:

Closing costs typically range from 2% to 5% of the loan amount. Most borrowers pay an origination fee, title insurance fee, and deed recording fee. You may also owe local taxes, which are inexpensive in some areas and quite costly in others. And some borrowers choose to prepay mortgage interest through points in exchange for a lower interest rate.

A closing cost unique to VA loans is the VA funding fee: on an IRRRL, the fee is 0.5%, or $500 for every $100,000 borrowed. You may be exempt if you’re receiving payments for a service-connected disability or you’ve earned a Purple Heart.

Rolling closing costs into your VA IRRRL

An IRRRL allows you to roll your closing costs into the loan. You might benefit from this option if

you stand to save a lot from refinancing but don’t have cash on hand. It can also be a smart move if you’re planning to sell your home the next time you get permanent change of station (PCS) orders. It probably doesn’t make sense to pay a lot up front for a loan you’ll have short term.

On a 30-year mortgage, here’s how much more you would pay over the life of the loan by rolling $12,000 in closing costs (4% of $300,000) into the loan instead of paying them up front.

| Interest rate | Pay closing costs up front | Roll closing costs into loan | Additional cost |

|---|---|---|---|

| 3% | $12,000.00 | $18,345.30 | $6,345,30 |

| 4% | $12,000.00 | $20,721.16 | $8,721.16 |

| 5% | $12,000.00 | $23,388.64 | $11,388.64 |

While inflation is normally seen as a bad thing, it can be good for mortgage debtors with fixed interest rates. As years pass, even modest price and income inflation can make your mortgage debt feel less expensive.

In other words, while an extra $6,300 may sound like a lot today, it’ll feel like less and less each year due to inflation. Still, the higher your interest rate, the less you may want to borrow.

How to apply for a VA IRRRL

If you apply for a VA IRRRL, the process will look something like this:

- Identify reputable lenders that offer a VA streamline refinance.

- Submit a pre-approval application online or by phone with at least three lenders.

- Compare your Loan Estimate from each company, looking for the best terms for your situation.

- Decide how many points to pay, if any, to lower your rate.

- When you’re happy with current interest rates, lock your rate.

- Submit any supporting documents your lender asks for. Your lender will usually be able to obtain your VA loan certificate of eligibility (COE) for you.

- Sign the paperwork to close on your loan.

Read: How Often Can You Refinance Your Mortgage?

Is a VA streamline refinance loan right for you?

Refinancing an existing home loan into a new loan may be a good idea if you’ll be able to lower your interest rate by at least one percentage point. It also makes sense if you expect to keep your new loan long enough to break even on closing costs.

A VA streamline refinance in particular may be right for you if you’ve lost your job, your credit score has dropped, your income has decreased, or your home’s value has declined. Since lenders aren’t required to order an appraisal or perform credit underwriting for an IRRRL, this type of refinance could help you keep your home if times have gotten tough.

If you plan to move soon or can’t lower your rate, refinancing may not help you. And if you have at least 20% equity, good credit, and a steady income, it’s worth comparing quotes for both an IRRRL and a conventional refinance.

No matter which type of refinance you decide to pursue, comparing offers from multiple lenders can help you save money. While Credible doesn’t offer VA loans, we can help you see customized, prequalified rates for a conventional refinance — checking rates with us won’t impact your credit score.

Keep Reading: How to Refinance Your Mortgage With Bad Credit