Federal Direct Unsubsidized Loans: Explained

Our goal is to give you the tools and confidence you need to improve your finances. Although we receive compensation from our partner lenders, whom we will always identify, all opinions are our own. Credible Operations, Inc. NMLS # 1681276, is referred to here as “Credible.”

College can be expensive — but the good news is that there are several funding sources that can help you cover your education costs, including both federal and private student loans.

There are a few types of federal student loans available to college students: Direct Subsidized Loans, Direct Unsubsidized Loans, and Direct PLUS Loans. If you need to borrow for school, it’s usually best to start with subsidized loans before turning to Direct Unsubsidized Loans and other options.

If you’re wondering how a federal Direct Unsubsidized Loan works, here’s what you should know:

What is a federal Direct Unsubsidized Loan?

Federal Direct Unsubsidized Loans are available to undergraduate, graduate, and graduate students regardless of financial need. This means that the majority of students can apply for them no matter what their financial situation is.

Learn More: Subsidized vs. Unsubsidized Student Loans: Know the Difference

Direct Subsidized Loans vs. Direct Unsubsidized Loans vs. Direct PLUS Loans

The right federal student loan for you will depend on your year in school and your financial need. If you’re an undergraduate student with financial need, it’s a good idea to rely on subsidized loans as much as possible before turning to unsubsidized loans and PLUS Loans.

Here’s how these three main types of federal student loans work:

- Direct Subsidized Loans are available to undergraduate students who demonstrate financial need. The government covers the interest on these loans while you’re in school.

- Direct Unsubsidized Loans are available to undergraduate, graduate, and professional students. Unlike subsidized loans, unsubsidized loans are considered non-need-based aid — which means you could qualify for them without financial need. However, keep in mind that you’ll have to pay all of the interest that accrues on unsubsidized loans.

- Direct PLUS Loans come in two categories: Grad PLUS Loans for students who want to pay for grad school and Parent PLUS Loans for parents who want to pay for their child’s education. These loans generally come with higher interest rates than subsidized and unsubsidized loans — and like unsubsidized loans, any accrued interest is your responsibility. PLUS Loans also require a credit check.

| Direct Subsidized Loans | Direct Unsubsidized Loans | Direct PLUS Loans | |

|---|---|---|---|

| Who qualifies? | Undergrad borrowers with financial need | Undergrad, graduate, and professional students (regardless of financial need) |

|

| Interest covered by the Department of Education |

|

None | None |

| Available to graduate or professional students? | No | Yes | Yes |

| Credit check required? | No | No | Yes, must not have an adverse credit history (or must have an endorser) |

| Fees | 1.057%* | 1.057%* | 4.228%* |

| Interest rates |

|

|

|

| Aggregate loan limits (for dependent students) |

|

|

Up to school’s cost of attendance (minus any other financial aid received) |

| Aggregate loan limits (for independent students) |

|

|

Up to school’s cost of attendance (minus any other financial aid received) |

| *Federal student loan rates and fees are for the 2021-22 academic school year. | |||

No matter what type of student loan you get, it’s important to consider how much that loan will cost you so you can prepare for any added expenses. For example, if you take out a Direct Unsubsidized Loan, you’ll need to take into account that you’ll pay more in interest.

Find out how much you’ll owe over the life of your federal or private student loans using our student loan calculator below.

Enter your loan information to calculate how much you could pay

With a $ loan, you will pay $ monthly and a total of $ in interest over the life of your loan. You will pay a total of $ over the life of the loan, assuming you’re making full payments while in school.

How to qualify for an unsubsidized loan

To qualify for a Direct Unsubsidized Loan, you must:

- Be a U.S. citizen or eligible noncitizen

- Be enrolled at least half time at a school that participates in the federal financial aid program

- Be enrolled in a degree- or certificate-granting program awarded by that school

- Have a valid Social Security number

- Have a high school diploma or equivalent (such as a GED)

Check Out: Federal Stafford Loans

How to get an unsubsidized loan?

If you want to take out an unsubsidized loan, follow these three steps:

1. Fill out the FAFSA

If you need to pay for college, your first step should be completing the Free Application for Federal Student Aid (FAFSA). Your school will use your FAFSA results to determine what federal student loans and other federal financial aid you qualify for.

Keep in mind that some financial aid is given on a first-come, first-served basis — so it’s a good idea to complete the FAFSA as early as possible, especially if you have high financial need.

2. Apply for scholarships and grants

Unlike student loans, college scholarships and grants don’t have to be repaid — which makes them a great way to pay for school. There’s no limit to how many scholarships and grants you can get, so it’s a good idea to apply for as many as you can.

- Nonprofit organizations

- Local and national businesses

- Professional associations in your field

You might also qualify for school-based scholarships, depending on your FAFSA results. Additionally, consider using websites like Fastweb and Scholarships.com to easily look for awards that you could be eligible for.

3. Take out federal student loans

If you need to borrow for school, it’s usually best to rely on federal student loans first. This is mainly because you’ll have access to federal student loan benefits — such as income-driven repayment (IDR) plans and student loan forgiveness programs.

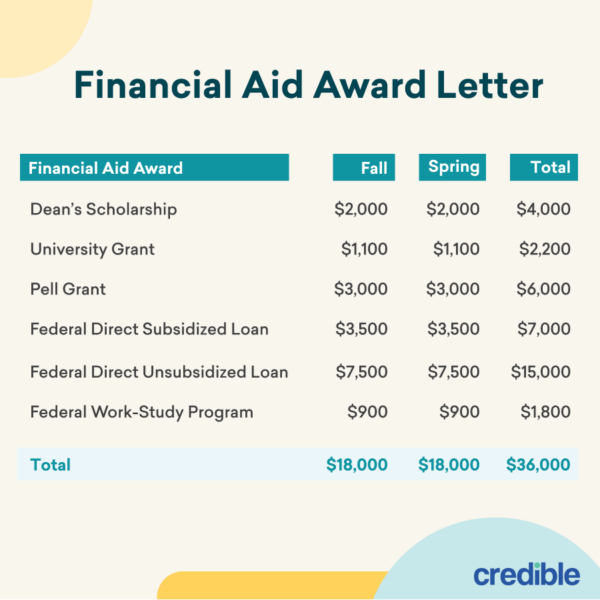

Once you complete the FAFSA, your school will send you a financial aid award letter detailing the federal student loans, federal financial aid, and school-based scholarships you qualify for. You can then choose which aid you’d like to accept. Here’s an example of how an award letter might look:

Loan fees for Direct Subsidized and Unsubsidized Loans

Federal student loans typically come with a disbursement fee. This is taken out of your loan amount when the funds are released to your school.

For the 2021-2022 academic year, this fee is 1.057% for both Direct Subsidized and Unsubsidized Loans — somewhat less than the 1.059% disbursement fee for the 2019-2020 academic year.

Learn More: Borrowing for College? Start with Subsidized Student Loans

How much can you borrow with an unsubsidized loan?

How much you can borrow with an unsubsidized loan depends on your year in school as well as if you’re a dependent or an independent student. Here are the student loan limits you can expect:

- Direct Subsidized Loans: $3,500 to $5,500 per year

- Direct Unsubsidized Loans (dependent undergraduate): $5,500 to $7,500 per year ($31,000 aggregate limit)

- Direct Unsubsidized Loans (independent undergraduate): $9,500 to $12,500 per school year ($57,500 aggregate limit)

- Direct Unsubsidized Loans (graduate or professional): $20,500 per year ($138,500 aggregate limit)

- Direct PLUS Loans: Up to your school’s cost of attendance (minus any other financial aid you’ve received)

Check Out: Federal vs. Private Student Loans: 5 Differences

Private student loans: When federal funding isn’t enough

It’s possible that scholarships, grants, and federal student loans might not be enough to fully pay for your education. In this case, a private student loan could be a helpful option to cover any remaining expenses.

But before you apply for a private student loan, it’s important to understand how they differ from federal student loans. Here are some of the key points to keep in mind as you weigh your options:

- Who offers them: Private student loans are provided by private lenders, including online lenders as well as traditional banks and credit unions.

- Interest rates: Rates on private loans are set by individual lenders according to market conditions. The rate you get will also depend on other factors, including your credit score as well as the repayment term you choose. With Credible partner lenders, fixed rates start at 2.94%+

, and variable rates start at 0.94%+

. - Repayment terms: You’ll typically have five to 20 years to repay a private student loan, depending on the lender. It’s usually best to choose the shortest term you can afford to keep your interest costs as low as possible. Many lenders also offer better rates to borrowers who opt for shorter terms.

- Credit requirements: Unlike most federal loans, private student loans require a credit check. To qualify, you’ll generally need good to excellent credit. A good credit score is usually considered to be 700 or higher. There are also some lenders that offer student loans for bad credit — but these loans usually come with higher interest rates compared to good credit loans.

- Benefits: Private student loans don’t come with federal protections, but they do offer some benefits of their own. For example, you can apply at any time, and you might be able to borrow more than you’d get with a federal loan. And if you have excellent credit, you could get a lower interest rate on a private loan compared to a federal loan.

- Drawbacks: A major drawback of private student loans is their lack of federal protections. For example, you won’t be able to sign up for an IDR plan or pursue federal student loan forgiveness.

A cosigner can be anyone with good credit — such as a parent, another relative, or a trusted friend — who is willing to share responsibility for the loan. Just keep in mind that they’ll be on the hook if you can’t make your payments.

If a private student loan seems like a good fit for your needs, be sure to consider as many lenders as possible to find the right loan for you. Credible makes this easy — you can compare your prequalified rates from our partner lenders in the table below in two minutes.

| Lender | Fixed rates from (APR) | Variable rates from (APR) | Loan amounts | Loan terms (years) | Min. credit score |

|---|---|---|---|---|---|

Credible Rating |

3.36%+ | 1.46%+ | $2,001 to $200,000 | 7 to 20 | 540 |

|

|||||

Credible Rating |

3.23%+1 | N/A | $1,000 to $350,000 (depending on degree) | 5, 10, 15 | 720 |

|

|||||

Credible Rating |

2.94%+2,3 |

0.94%+2,3 | $1,000 up to 100% of the school-certified cost of attendance | 5, 8, 10, 15 | Does not disclose |

|

|||||

Credible Rating |

3.2%+ | 1.03%+ | $1,000 to $99,999 annually ($180,000 aggregate limit) |

7, 10, 15 | Does not disclose |

|

|||||

Credible Rating |

3.02%+7 | 2.37%+7 | $1,000 to $200,000 | 7, 10, 15 | 750 |

|

|||||

Credible Rating |

3.33%+8 | 1.69%+8 | $1,001 up to 100% of school certified cost of attendance | 5, 10, 15 | 670 |

|

|||||

Credible Rating |

3.75%+ | N/A | $1,500 up to school’s certified cost of attendance less aid | 15 | 670 |

|

|||||

Credible Rating |

3.5% – 12.6% APR9 | 1.13% – 11.23% APR9 | Up to 100% of the school-certified cost of attendance | 15 | Does not disclose |

|

|||||

| Compare private student loan rates without affecting your credit score. 100% free!Compare Private Loans Now |

|||||